All Articles about Battery Storage

The value proposition of battery storage extends far beyond mere wholesale energy arbitrage. To truly unlock the full economic potential of these assets and maximize their contribution to grid stability, it is crucial to consider their participation in ancillary services markets. We show this multi-market optimization here by way of example focusing on all spot markets (Day-Ahead, Intraday and Intraday Continuous) as well as the ancillary services.

The Hamburg-based power trader, direct marketer, and power supplier CFP FlexPower has founded an independent subsidiary to expand the development and operation of grid-connected large battery storage systems in Germany. The new company, FlexPower Energy, focuses on providing energy storage systems rated between two and 50 megawatts of power.

Battery energy storage systems are becoming a cornerstone of Germany’s energy transition. We explore the financial opportunities and risks in Germany’s wholesale and balancing markets.

With Germany on the brink of a pivotal election, we want to share our high-level views on energy policy and the key considerations for voters. We’ve outlined five fundamental theses to keep this concise and to the point.

Electricity (cross-product) price volatility has historically been closely linked to overall price levels. This trend seems to have ended in 2024 in Germany, as low marginal cost renewables are pushing the overall wholesale price level down, while peakers such as gas and batteries need to finance their investments in relatively few but increasingly expensive production hours

FlexPower GmbH, PowerField Energy B.V., and Spectral have commenced trading operations for the co-located Battery Energy Storage System (BESS) and Photovoltaic (PV) plant in Wanneperveen.

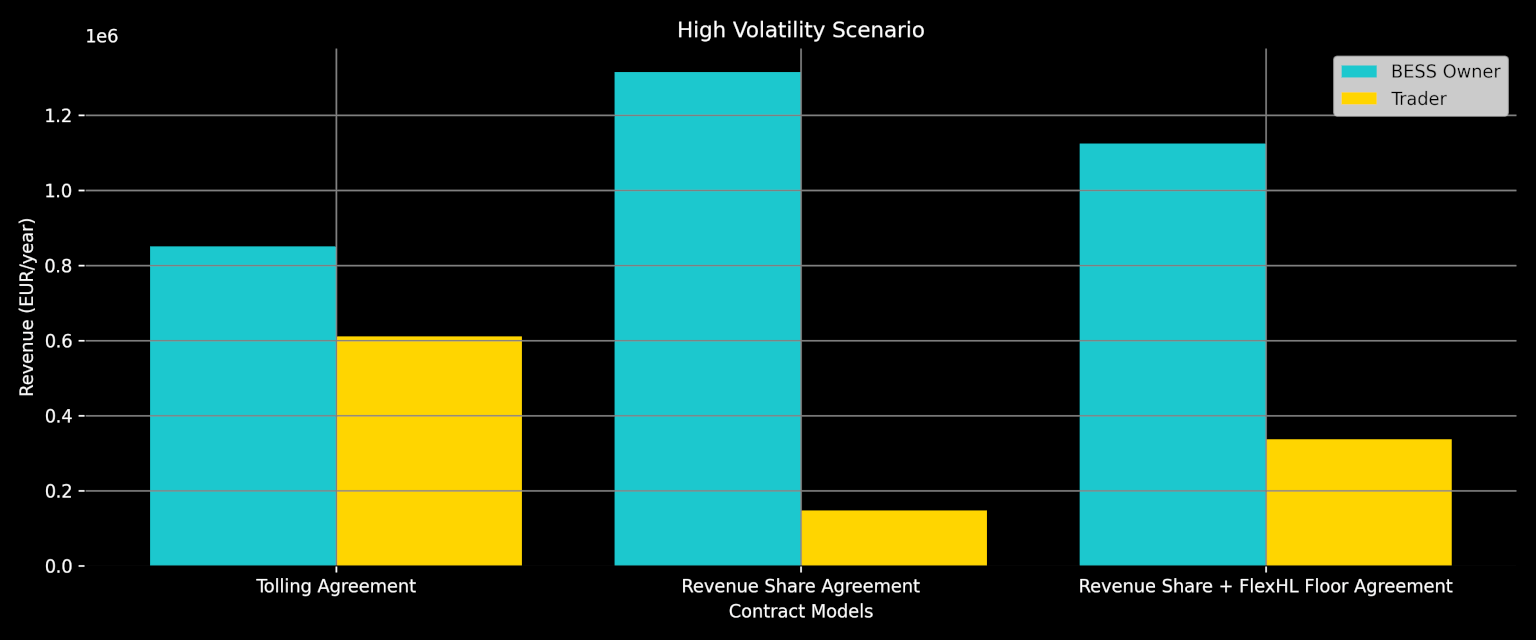

This blog post is the third in a series of articles about hedging price volatility using standard shapes such as wind and PV, as well as more novel and somewhat non-standard ones, such as the FlexHL (Battery). While the first two articles were explainers for consumers, this one is for suppliers who are looking to sell their flexibility, i.e. BESS owners.

In this subsequent blog, we extend our discussion from part I and look at how to use Flex HL (battery) shapes to hedge against price volatility.

The FlexIndex measures on a daily basis the revenues that operators of flexible assets can achieve in Germany’s short-term spot market. The index is based on a reference battery with a storage capacity of one megawatt-hour and a power of one megawatt.

Over the last year we became increasingly involved with the “science” of modelling past and future revenues of battery energy storage systems (BESS) and now decided to shed some light on this practice. We believe that customers are being sold a lot of voodoo for science and that the incentives in this industry are not at all well aligned.